The Gigawatt Gap

A structural power deficit is quietly derailing the $7 trillion AI buildout

The United States is spending trillions of dollars building the most sophisticated AI infrastructure in human history. Hyperscalers are committing $500 billion, $600 billion, even $700 billion to data centers, chips and compute clusters every year. Every major investment bank has a slide deck titled some version of “The AI Arms Race.” And yet, as the concrete gets poured and the servers get racked, a deeply uncomfortable question keeps surfacing:

Where, exactly, is all the electricity going to come from?

This is not a theoretical problem. It is a structural deficit that is already derailing projects, inflating utility bills, generating political backlash across the ideological spectrum and, most importantly, threatening America’s ability to maintain its lead in the most consequential technology competition of the 21st century. The grid is not ready. The question is what, if anything, can be done about it and how fast.

The Numbers Are Staggering

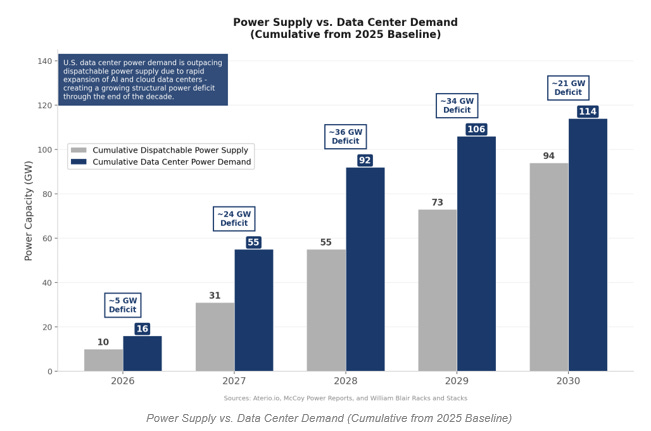

According to data compiled by multiple sources, U.S. data center power demand is set to outpace dispatchable power supply on a cumulative basis throughout the rest of the decade. The deficit peaks at approximately 36 GW in 2028 before compressing modestly to around 21 GW by 2030, but make no mistake, there is no scenario where supply catches demand before 2030 without radical intervention.

To put 36 GW in context: that is roughly the equivalent of 36 large conventional power plants running at full capacity around the clock. It is more than the entire installed generating capacity of countries like Colombia or the Netherlands. This is not a rounding error. This is a structural mismatch between capital ambition and physical infrastructure.

The consequences are already manifesting. According to ZeroHedge and multiple industry sources, 30 to 50 percent of large U.S. data centers scheduled to open in 2026 will be delayed or canceled. Of the 12 to 16 gigawatts of U.S. capacity planned for 2026, only approximately 5 gigawatts is actually under construction. As of mid-2025, more than 36 projects representing $162 billion in cumulative investment were either blocked or significantly delayed, not because of capital, not because of permitting alone, but because of the inability to connect to a grid that simply cannot handle the load.

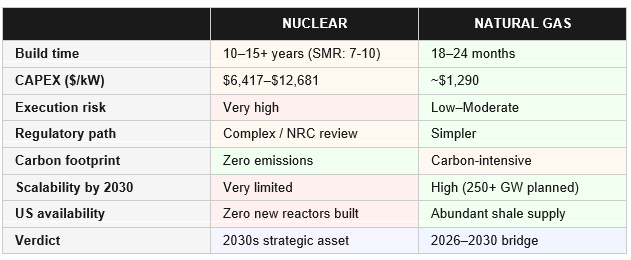

Option A: Nuclear — The Premium, Long-Dated Play

The intellectual case for nuclear power as the backbone of AI infrastructure is compelling. It is dispatchable, unlike solar and wind, it delivers baseload power 24 hours a day, 365 days a year. It is carbon-free, which matters both for ESG-sensitive hyperscalers and for long-term regulatory risk. And it is energy-dense in ways that no other clean source can match.

Big tech has noticed. Microsoft signed a 20-year, $16 billion agreement to restart Three Mile Island’s Unit 1 (835 MW, targeting 2028). Google signed the first U.S. corporate SMR fleet deal with Kairos Power for 500 MW by 2030+. Amazon is backing 5 GW of X-energy SMR deployments by 2039. Meta has contracted for up to 8 Natrium reactor plants, with initial delivery as early as 2032.

These are serious commitments. The problem is the timeline.

No SMR is commercially operating in the United States today.

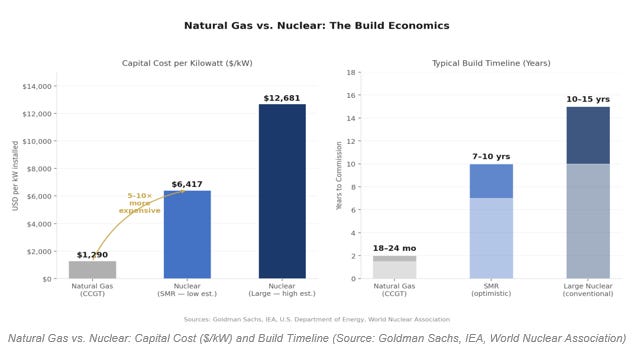

Goldman Sachs estimates that nuclear CAPEX runs $6,417 to $12,681 per kilowatt, versus $1,290/kW for natural gas. That is a 5x to 10x capital premium, before accounting for the decade-plus construction timeline.

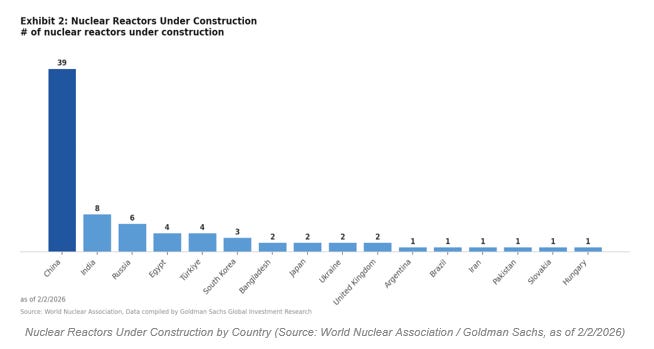

The nuclear story is real. But for the window between now and 2030, precisely the period during which the AI infrastructure buildout is most capital-intensive and most urgent, nuclear simply cannot be the primary answer. The United States has zero new large-scale reactors under construction and no national-level mobilization underway to change that math in any meaningful near-term timeframe.

Option B: Natural Gas — The Pragmatic, Scalable Bridge

If nuclear is the premium long-dated bond, natural gas is the floating rate note: imperfect, carbon-intensive, but available now.

The build-time comparison is not even close. A combined-cycle natural gas plant can be commissioned in 18 to 24 months. One was reportedly built in four months. Compare this to 10–15 years for a conventional nuclear reactor, or 7–10 years for an SMR under the most optimistic projections. For a technology industry operating on quarterly earnings cycles and annual CAPEX guidance, this differential is decisive.

The economics also favor gas. At approximately $1,290 per kilowatt of installed capacity versus nuclear’s multi-thousand dollar range and with the U.S. sitting atop one of the world’s largest natural gas reserves thanks to the shale revolution, the input cost structure is fundamentally more attractive. Execution risk is lower, the regulatory pathway is cleaner and the technology is proven at scale.

The market is already voting with capital. Proposals for new natural gas-burning facilities in the U.S. tripled in 2025 compared to 2024. The U.S. is now planning more than 250 GW of new natural gas capacity, much of it driven by hyperscalers building their own captive generation. Microsoft is developing a plant with Chevron and Engine No. 1 in West Texas that could reach 5 GW. Google confirmed construction of a 933 MW natural gas plant in North Texas with Crusoe Energy.

This is not the clean energy narrative Silicon Valley likes to project. But it is the reality of what happens when the grid cannot move fast enough and the AI CAPEX machine cannot wait.

There is one important supply-side caveat: turbine manufacturers are so backlogged that new gas turbine orders reportedly cannot be placed until 2028, with delivery timelines extending to six years. The companies that secured turbine orders early are insulated; those that didn’t face a different kind of bottleneck.

Side-by-Side: Nuclear vs. Natural Gas

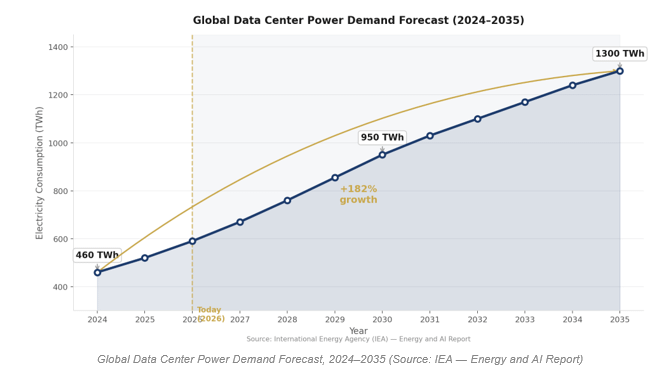

The honest assessment of the 2026–2030 window is this: natural gas will bear the majority of incremental load growth for AI infrastructure. It is the only scalable, deployable, cost-competitive option that can move fast enough to match the demand curve. The IEA projects that natural gas and coal together will meet over 40% of additional electricity demand from data centers through 2030.

Beyond 2030, the calculus begins to shift. SMR technology will mature, early commercial deployments will de-risk the asset class and the carbon economics of continued gas expansion will face increasing headwinds, regulatory, political and market-driven. Nuclear’s premium will remain, but its strategic value as zero-emissions baseload will appreciate alongside increasingly ambitious climate commitments.

The real policy failure is the absence of a national plan that sequences these two realities: gas as the bridge, nuclear as the destination.

What the U.S. currently has is a chaotic, market-driven scramble with no coordinated infrastructure doctrine.

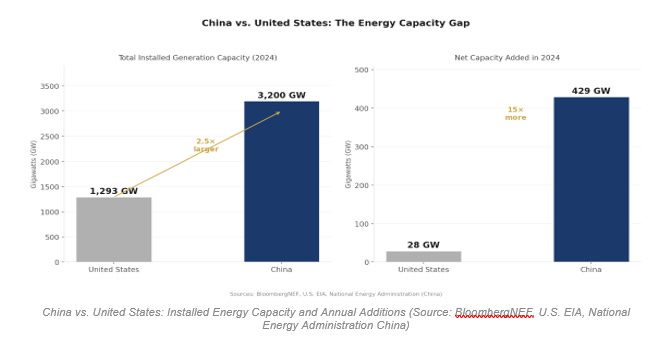

China Is Playing a Different Game

While the United States debates gas versus nuclear at the margin, China is deploying both, at scale, simultaneously and without the friction of a contested democratic regulatory process.

China’s installed electricity generation capacity stands at approximately 3,200 GW, versus 1,293 GW for the United States. In 2024 alone, China added a net 429 GW of electric generation capacity, more than 15 times the net capacity added by the U.S. in the same year. Bloomberg projects China will add more than 3.4 terawatts of new generation over the next five years, nearly six times as much as the U.S.

On nuclear specifically: China currently has 39 reactors under construction (per World Nuclear Association), representing more than half of the entire global nuclear construction pipeline. The U.S. has zero. China is not choosing between gas and nuclear. China is building everything, everywhere, all at once.

The U.S. controls approximately 74% of global high-end AI compute today. But compute without power is stranded capital.

If the energy gap is not closed, the compute advantage erodes, not because China surpasses the U.S. in chips, but because the U.S. cannot turn those chips on fast enough.

Brazil: Clean Energy Abundance, Regulatory Uncertainty

There is an often-overlooked wildcard in this story: Brazil.

Brazil generates 93.6% of its electricity from renewables, with approximately 80% from hydropower alone. It possesses nearly one-fifth of the world’s freshwater reserves, critical not only for power generation but for data center cooling. Microsoft has committed $2.4 billion to Brazilian cloud and AI infrastructure; Amazon Web Services is investing $1.8 billion through 2034.

A RAND Corporation report published in April 2025 explicitly framed U.S.-Brazil AI cooperation as a strategic opportunity: American semiconductor technology in exchange for Brazilian renewable energy, a “Digital Dams” framework. In a world where the U.S. faces a structural power deficit and Brazil has abundant, clean, dispatchable energy, there is a natural basis for a bilateral AI infrastructure partnership. Certain categories of compute workloads, training runs, inference clusters, hyperscale storage, do not have to be physically located in the continental United States.

The obstacle is regulatory. Brazil’s government launched Redata in September 2025, a special tax regime for data centers tied to environmental commitments, designed to fast-track foreign investment. Then, in February 2026, Redata expired after failing to secure congressional approval. Brazil’s AI regulatory framework (Bill 2338) has passed the Senate but remains stuck in the House.

Brazil’s energy abundance is real. Its political will to build the regulatory scaffolding around it remains the open question.

The Backlash No One Wants to Talk About

There is a final dimension to this story that is being systematically underreported in the context of AI investment narratives: the political economy of electricity pricing.

PJM Interconnection, the largest electricity market in the U.S., saw the cost of its annual capacity auction jump from $2.2 billion for 2024-2025 to $14.7 billion for 2025-2026, an increase of more than 500%. An independent monitor attributed 63% of that increase directly to data center demand. Residential electricity prices rose approximately 5% in 2025 and are forecast to rise another 4% in 2026.

The political consequences are already non-trivial. Senator Bernie Sanders and Florida Governor Ron DeSantis, two politicians who agree on virtually nothing, have both spoken out against the data center buildout. In Q2 2025, data center opponents slowed or thwarted projects totaling roughly $100 billion, more than any single quarter since 2023. Microsoft disclosed to investors that community opposition is now a material risk to its expansion plans.

The hyperscalers capture the upside of AI infrastructure. Ordinary ratepayers absorb the cost of the grid upgrades required to power it.

That tension is not going away. If anything, it will intensify as the deficit widens and electricity prices continue to climb.

The Bottom Line

Natural gas wins the 2026–2030 window. It is faster to build, cheaper to deploy, and available at the scale the market requires.

Nuclear wins the next decade. The SMR pipeline is real, but it is a 2030s story at the earliest. The U.S. needs to begin building today, at the national policy level, what it will need operationally in 2033.

China is not waiting. With 3x U.S. installed capacity and 39 reactors under construction, China is executing a comprehensive energy-plus-AI strategy that the U.S. has no coherent answer to.

Brazil is a strategic opportunity, not yet a strategic partner. The energy is there. The political framework is not, yet.

The United States built the interstate highway system in a decade. It landed on the moon in less than that. The energy infrastructure required to sustain AI leadership is not a more complex engineering problem than either. What it requires is the same thing those projects required: urgency, coordination and political will.

Can natural gas realistically bridge the gap to 2030 or is the U.S. already too far behind? And is China’s energy advantage a strategic threat to American AI dominance or is U.S. compute superiority a sufficient offset? This is exactly the kind of macro-structural question where we consistently produce the sharpest thinking.

Disclaimer: This content is for informational purposes only and does not constitute investment advice. Always conduct your own due diligence.

Souces: Goldman Sachs, ZeroHedge, Fortune, CNBC, Brookings, IEA, Marketplace, JP Morgan, Bloomberg, Morgan Stanley, UBS, TechCrunch, Rand.

Interesting take—I’ve been looking at this from a similar angle, especially around performance per watt and how efficiency is starting to matter more than raw speed. I recently wrote a breakdown comparing AMD and Intel if you’re interested.

Love the Article!

$IREN is a 100% renewable data center company with 4.5GW secured renewable grid-conected capacity.

Also I like the LNG and nuclear scenario, I think that in both of this Argentina is being overlooked.

With the world’s second largest technically-recoverable shale gas reserves. And a nuclear sector developing SMR for export.

All this I wrote in my newest article.