The Brazil Setup Update: What Changed in 30 Days And Why the Thesis Just Got Even Cheaper

The setup didn't break. The price did. That is not the same thing and the distinction is where the alpha lives.

Thirty days ago I published The Brazil Setup, laying out the macro case for a structural rotation into Brazilian equities and the five single-stock ideas I believed best expressed it. The tape since then has done its best to embarrass me and I feel responsible to address the subject now.

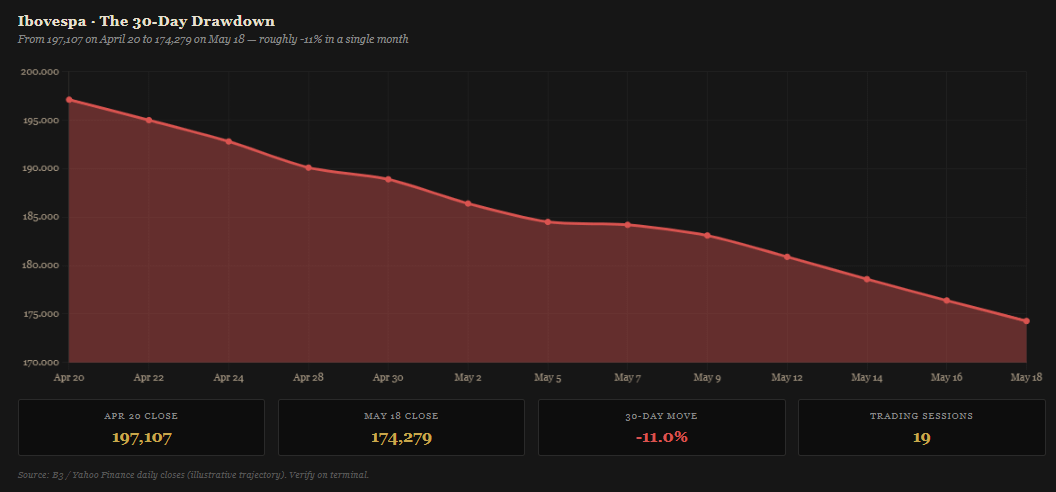

The Ibovespa has fallen roughly 11% in a single month, sliding from 197,107 points on April 20 to 174,279 by May 18. Foreign portfolio flow has flipped from the strongest accumulation pace since 2021 to a violent reversal: net foreign outflows of roughly R$23 billion from April 15 through May 18, an almost mechanical sale every single trading day of the window. EWZ has retraced. The Real has come under pressure on the back of the outflow. The five names I named have all repriced lower.

What the market is processing right now is: what changed?

Because the answer matters. If the fundamental thesis is broken, you sell and you do not look back. If the price is broken but the thesis is intact, or, more interestingly, if the price is being broken by global factors that have nothing to do with Brazilian fundamentals, then you have just been handed a better entry into the same trade.

I will tell you upfront where this piece lands, so you can decide whether to keep reading: the thesis is not broken. The price is. And the disconnect is widening, not narrowing. What follows is the work.

A reminder on positioning: I write from inside the Brazilian market, not about it. São Paulo-based, watching the political news cycle in real time, reading the local press alongside the Bloomberg terminal, and, as I disclosed in the prior piece, a client of several of the institutions I cover. That ground-truth read is what allows me to separate the noise from the signal in moments like this, when foreign-media narratives and local reality drift apart.

Part I — What Actually Happened

Six things moved at once. None of them were Brazilian in origin and that’s the most important fact in this entire piece.

1. The Global Long End Broke Out

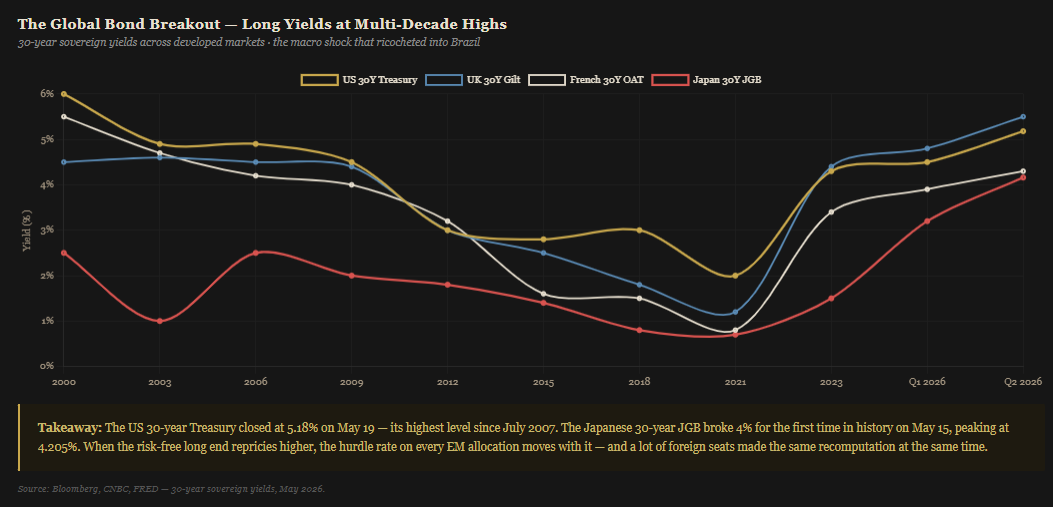

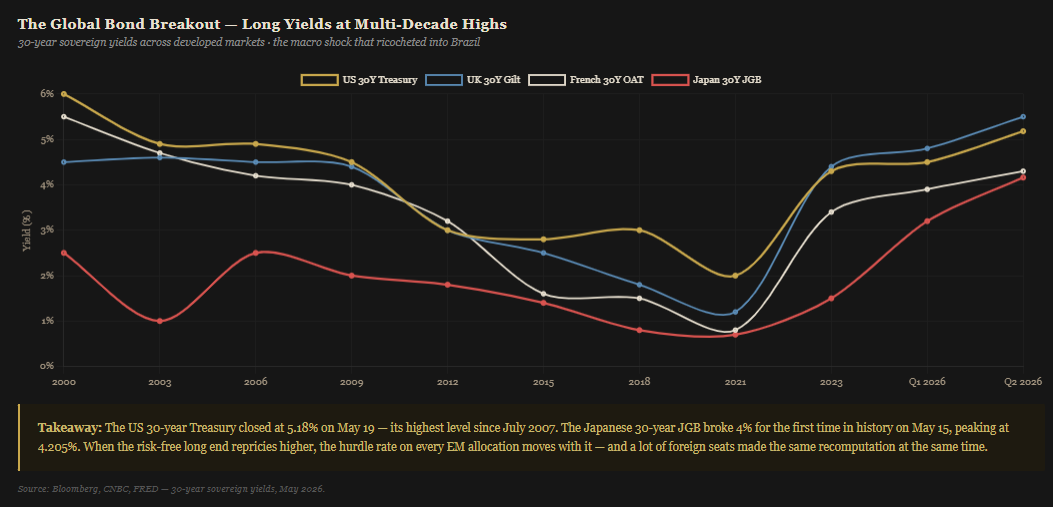

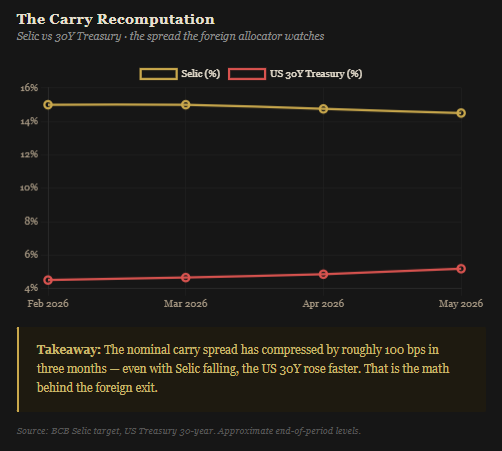

The defining macro event of the last 30 days is not Brazilian. It is the breakout in developed-market long bond yields.

The US 30-year Treasury yield closed at 5.18% on May 19, briefly tagging 5.19% intraday, the highest level since July 2007, a 19-year high. The 10-year has moved from roughly 3.96% in February to 4.68% in May.

The Japanese 30-year JGB yield broke 4% for the first time in a lot of years on May 15, peaking at 4.205%, a structural rupture in a market that has anchored global term premia for two decades.

French OATs and UK Gilts at the 30-year point are at multi-decade highs in their own right.

This is not a US story. This is a synchronized global repricing of duration, driven by a confluence: persistent fiscal slippage in the major sovereigns, oil-driven inflation impulse from the Iran conflict, the Sanae Takaichi administration’s fiscal expansion in Japan and a Bank of America fund manager survey showing 62% of respondents now expect the 30-year Treasury to hit 6%, the highest expectations reading since late 1999.

Why this matters for Brazil: when the risk-free long end repricies higher, the hurdle rate on every EM allocation rises with it. A foreign investor looking at a Brazilian Interest Rate of 14.50% does the math against a 5.18% 30-year Treasury, not a 4.50% one. The carry premium compresses. The currency hedging cost moves. The decision to own Brazil instead of duration in your own currency gets recomputed in real time and a lot of seats made the same recomputation at the same time.

2. The Iran War Refuses to End

In Iran War: Three Scenarios I sketched the paths this conflict could take and the macro implications of each. Two months in, what we have is the worst combination for global risk assets: a fragile ceasefire that keeps unravelling, with oil refusing to settle. Brent has been whipsawing between roughly $100 and $115 per barrel through May, and every flare-up in Hormuz repricies the global inflation curve in the wrong direction.

This feeds back directly into Point 1: the longer oil stays elevated, the longer the term premium has to stay in the long end of every developed-market sovereign curve. The Trump administration keeps signalling a near-term resolution; the negotiations keep dragging. The market is now positioned for the bad-case duration on this conflict, not the good-case.

3. The S&P 500’s “All-Time High” Is a Mirage

This one matters because it explains where the marginal global capital is and is not going.

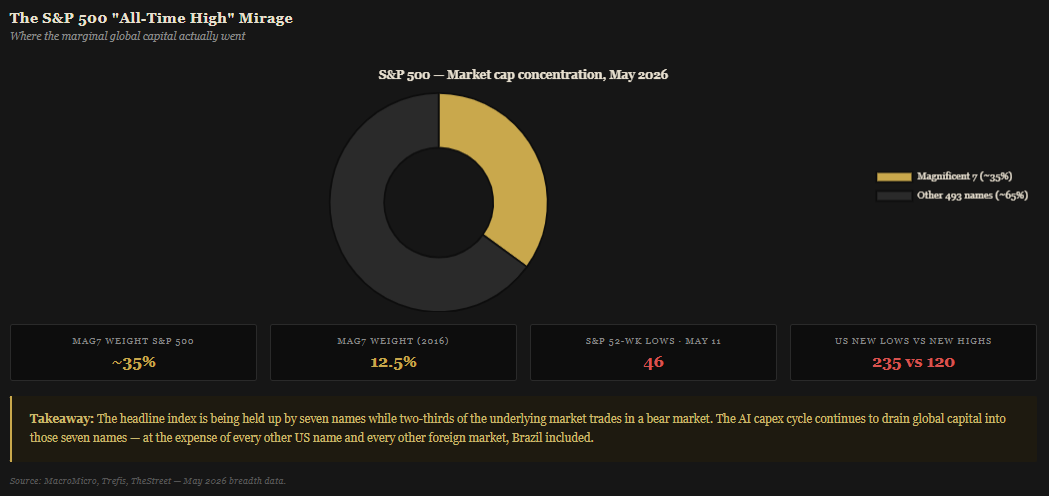

The S&P 500 has continued to print at or near all-time highs through this drawdown elsewhere. On the surface, that signals risk-on appetite. Underneath the surface, breadth has collapsed, which I didn’t anticipate.

The Magnificent 7 now account for roughly 35% of the S&P 500’s market capitalization, up from 12.5% a decade ago.

On May 11 alone, 46 individual S&P 500 names hit a 52-week low, on the same day the index sat near record highs.

New 12-month lows are running roughly 235 versus 120 new 12-month highs across US listings. That is a bear market in two-thirds of the index masquerading as a bull market in the headline.

This is the central tape illusion of 2026: the index is being held up mostly by seven names and the AI capex cycle continues to drain global capital into those seven names. When MAG7 earnings rip, every other US name and every other foreign market gets thinned. Brazil, a market with no AI exposure, a heavy commodity tilt and a 14.50% policy rate was always going to be on the receiving end of that capital rotation when momentum re-asserted in late April.

4. Brazilian Politics Took a Hard Hit

This is the one that is local and it matters more than the foreign press has fully digested.

In the original Brazil Setup I flagged the 2026 presidential election as a potential fiscal reset catalyst: polling had consistently shown the center-right opposition ahead, and the leading opposition candidates had built their platforms on fiscal orthodoxy. The market was pricing a non-trivial probability of a regime change that would stabilize the debt trajectory.

That probability just got marked down. Senator Flávio Bolsonaro, until recently a meaningful contender in opposition polling, has been drawn into a scandal involving Banco Master and its former owner Daniel Vorcaro, who has been criminally charged with fraud. The Atlas poll commissioned by Bloomberg confirms it: Bolsonaro’s support has dropped sharply in the latest read.

I want to be careful here, because this is exactly the kind of nuance foreign coverage tends to flatten: the opposition is not Flávio Bolsonaro alone. There are other candidates. The center-right structural setup has not collapsed. But the probability-weighted expectation of a fiscally orthodox 2027 administration has been re-rated lower, and the market has priced that adjustment immediately. The election is still five months away. A lot can happen. But the easy “the opposition wins, fiscal stabilizes” call is harder to make today than it was 30 days ago.

5. The Carry Math Got Worse

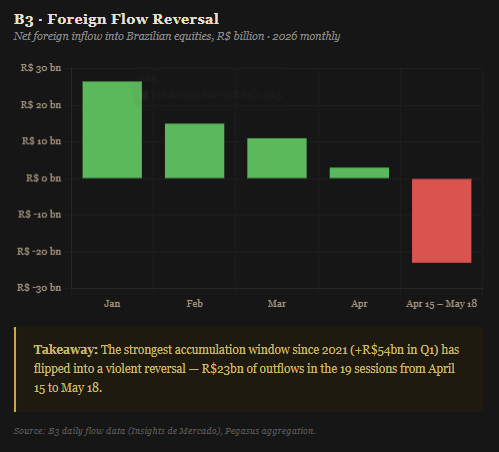

Combine Point 1 and Point 4 and you get the third-order effect: the carry trade narrative that brought R$54 billion of foreign capital into B3 between January and March suddenly looks less compelling.

The numbers track this almost perfectly. Foreign flow into B3 in 2026:

January: +R$26.5 billion (largest monthly inflow since January 2022)

February: +R$15 billion

March: +R$11 billion

April: +R$3 billion (sharp deceleration)

April 15 – May 18: roughly -R$23 billion (sustained, almost daily, outflow)

What changed in late April? Not Brazilian fundamentals, since Brazilian companies delivered first-quarter results that exceeded market expectations, lifted by still-strong economic activity at home and a better-than-expected rebound among exporters, despite rising costs continued to weigh on profit margins. The Treasury 30-year moved from roughly 4.50% to 5.18%. The JGB long end broke 4%. Iran refused to settle. The Flávio Bolsonaro story broke. Each one, on its own, marginal. Stacked, they re-rated the opportunity cost of being long Brazil for every global allocator simultaneously. When the long end of risk-free duration pays 5%-plus and the Bank of America survey says 62% expect 6%, the question “does Selic at 14.50% compensate me for FX risk plus fiscal risk?” gets a different answer than it did in January.

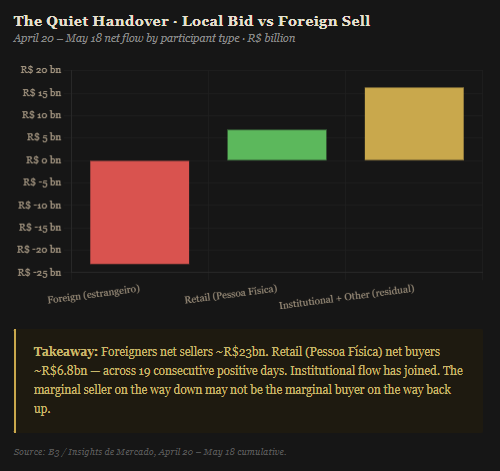

6. The Domestic Capital Quietly Stepped In

This is the part of the data that foreign press is missing entirely, and that I think is the most underappreciated signal in the market right now.

Through the same window of foreign outflows, Brazilian domestic capital has been a net buyer every single day. The B3 retail-investor data shows a 100% positive day count over 19 sessions from April 20 to May 18, with net domestic retail inflows of R$6.82 billion. Institutional flows tell a similar story.

Let me restate that, because it is the kind of detail that gets lost: retail investors in Brazil, historically allergic to equities, hammered by a 14.50% risk-free alternative, have bought stocks on every single one of the last 19 trading days. And institutional money has joined them. The foreigner is selling. The local is buying. Vigorously.

There is exactly one way to read that price action: the people closest to the assets see something the marginal foreign seller does not. That doesn’t mean they are right. But in my experience, when local money is accumulating into a foreign-led selloff in a market that is already trading at a deep discount to its global peers, that is signal, not noise.

Part II — Why This Sets Up Better, Not Worse

Here is the part that matters for the thesis.

The Macro Drivers Are Global, Not Brazilian

Look back at the six factors above. Number 1 is global. Number 2 is global. Number 3 is global. Number 5 is the second-order effect of 1 and 2. Number 6 is positive.

Only Number 4, the political reprice, is genuinely Brazilian in origin. And even there, the read is: the probability of a fiscal-reset catalyst has been marked down, not eliminated. The base case for Brazilian fiscal sustainability never required Flávio Bolsonaro specifically; it required any outcome that re-anchored expectations on the spending framework. That path is narrower today but not closed.

Five-sixths of what hit the tape was imported. If you believed Brazil at 197,000 points was an attractive structural long because of strategic endowments, real-rate asymmetry, valuation gap, and chokepoint-free commodity exposure, none of those facts changed in the last 30 days. The earnings season for Brazilian large caps in Q1 actually came in constructive. The interest rate was cut from 14.75% to 14.50% on April 29, deepening the easing cycle by another 25 basis points. The companies are operating as advertised.

The price moved. The fundamentals did not.

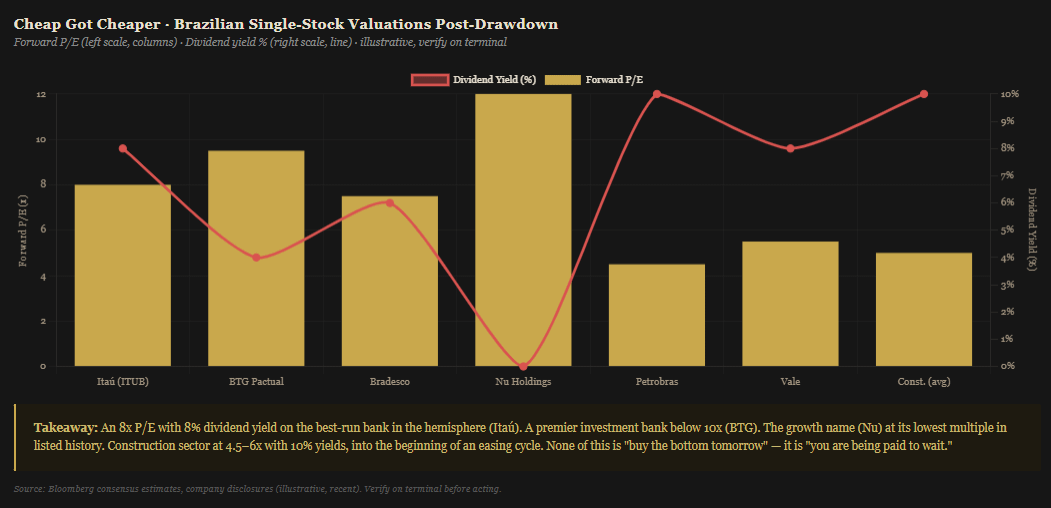

Cheap Got Cheaper

This is where the math becomes interesting. The forward multiples on the names I highlighted in Brazil Setup were already at the low end of the global cross-section. After an 11% drawdown in the index, with high-beta names selling off more, they are now extreme. Some snapshots from current screens:

Itaú Unibanco (ITUB) — trailing P/E in the 8x range, dividend yield around 8%, on a franchise that prints 20%+ ROE through the cycle. There is no major bank globally with that combination.

Banco BTG Pactual — trading below 10x P/L, which for a top-tier investment bank with a structurally growing wealth-management franchise is rare.

Nu Holdings (NU) — P/L near 12x, the lowest multiple in the stock’s listed history. A growth franchise being priced as a mature one.

Construction sector — broadly 4.5x to 6x earnings, dividend yields in the 10% area, with an interest rate that has started to come down and book value still compounding.

Petrobras (PBR) — still operating at a 60% discount to the Western majors, now with even more cushion built into the multiple after the recent retracement.

I want to flag the obvious counterpoint immediately: cheap can get cheaper. The lesson of every credit-tightening cycle is that compressed multiples can compress further when global liquidity exits. The market doesn’t ring a bell at the bottom. None of the above is a “buy the index tomorrow” call.

But here is the second-level frame: when you are owning a top-three Brazilian private bank at 8x earnings with an 8% dividend yield, you are not being paid to time the bottom. You are being paid to wait. The carry is real. The earnings power is real. The moat is real. And the marginal seller is a foreign allocator reacting to a Treasury yield, not to a Brazilian earnings miss. That mismatch is precisely the kind of dislocation that compounds well over multi-year windows.

The Domestic Bid Is a New Variable

I want to come back to Point 6 because I think it is structurally important and underweighted in the foreign discussion.

For most of the last decade, the Brazilian retail investor stayed out of equities. The reasons were rational: a brutal 2015-2016 recession, the impeachment, the 2018-2022 fiscal noise, and most importantly a real yield on government paper that paid you double digits in many windows for doing nothing. Why own stocks when Tesouro Selic paid 12%-plus with no volatility?

What is happening now is, in slow motion, a regime shift. With the easing cycle underway, the marginal saver is starting to look past the front of the curve. Retail equity buying for 19 consecutive sessions is not a normal observation in Brazilian market history. It coincides with a broader trend: pension fund allocations to equities slowly rising, family offices reducing their overweight in fixed income, and a steady stream of corporate dividend announcements bringing yield-seeking domestic capital into the equity market.

This is exactly the kind of structural rotation that creates a floor under valuations independent of foreign flow. If the foreign seller is the marginal price-setter on the way down, the domestic buyer is the marginal price-setter on the way back up. We may be watching the handover in real time.

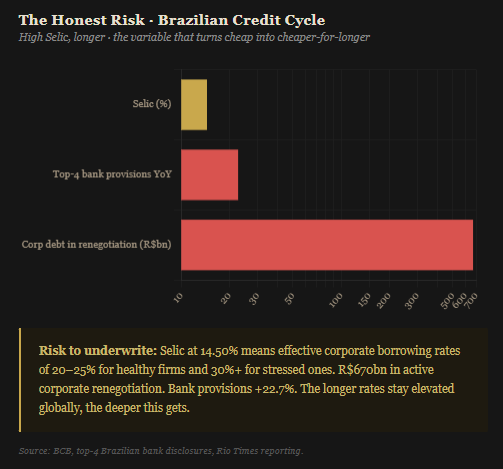

The Credit Backdrop Deserves Honest Disclosure

I want to be straight about the bear case, because the global credit picture is genuinely worse than it was 30 days ago and that deserves to be priced.

Brazilian banks raised loan-loss provisions by 22.7% to R$170.2 billion at the four largest names in the latest reporting cycle. Corporate debt in active renegotiation in Brazil has reached approximately R$670 billion, roughly 10% of total corporate credit stock, equivalent to about USD 116 billion at current rates. That is not nothing. With the interest rate at 14.50% and risk spreads on top, effective corporate borrowing rates run 20-25% for healthy companies and 30%-plus for distressed ones. The longer its stays elevated, the more this number grows.

The US distressed credit picture is no better: tech sector distressed debt alone reached roughly $46.9 billion by early February, and Apollo’s flagship BDC has seen non-accrual loans triple year-over-year from roughly $48.5 million to $167 million. Fitch puts the US private credit default rate at 5.8%, the highest in years. This is one of the threads I have been pulling on across the publication: the private credit and leveraged-loan ecosystem is starting to crack and the cracks compound when the long end of the curve refuses to come back down.

Why is this in the Brazil piece? Because credit cycles are the variable that turns “cheap” into “cheaper-for-longer.” Brazilian banks are well-capitalized and have weathered worse, but the longer high rates stay in the system globally, the higher the tail risk on the corporate credit cycle. This is a risk I would underwrite explicitly when sizing the trade, it is not a reason to avoid it, but it is a reason to scale in rather than back up the truck.

Part III — What I’d Actually Do

Three honest reads on positioning. I’ll keep this short because the work is in Parts I and II.

1. The long-term setup is more attractive than it was 30 days ago, not less. Strategic endowments, real-rate asymmetry, no chokepoint risk, functioning democracy, an easing cycle underway, and now an 11% lower entry point. That is a strictly better risk/reward than the April version of the same trade, provided you can stomach the path.

2. The short-term tape is hostile and likely to remain so until at least one of three things changes: (a) the US long end stabilizes, (b) the Iran conflict resolves or escalates definitively, or (c) Brazilian political polling reconverges around a credible fiscal-orthodoxy candidate. None of those is imminent. The bottom is rarely a date you can mark on a calendar.

3. Scale in. Don’t time it. The names that were attractive at 197,000 are more attractive at 174,000. They will be even more attractive if we see 165,000. The right posture, in my view, is tranched entry, a first tranche now, defined add-on triggers at lower levels, and discipline around position sizing. The Howard Marks lesson applies here as much as anywhere: the time to be aggressive is when the consensus has turned defensive. We are in that zone, not at the bottom of it.

A specific honest admission: I do not know when the selling stops. Anyone who tells you they do is selling something. What I do know is that asymmetric setups get more asymmetric as price moves against the consensus while fundamentals hold. That description fits Brazil better today than it did at the publication of the original piece.

Final Thought: The Setup Got Better Because the Price Got Worse

The most useful thing you can do as an investor, most days, is separate the signal from the price action. The Brazilian market is selling off because the global cost of capital just repriced higher and a political probability got marked down. It’s not selling off because Brazilian companies missed earnings, the easing cycle reversed, fiscal slipped further, or the commodity complex broke.

When the price moves against you on factors that are external to your thesis, the right question is not “should I sell?” The right question is “is the thesis still true at a better price?” In this case, my honest answer is yes, with the credit-cycle caveat above honestly priced into how you size it.

I would rather buy Itaú at 8x earnings and 8% yield with a foreign-led selloff in progress than buy Itaú at 10x and a thinner yield with everyone agreeing it’s a great trade. The hardest moments are usually the most profitable ones and the consensus rarely walks you to the entry.

For now: the foreigner is leaving, the local is buying, the fundamentals are intact and the discount has widened. That is the trade.

What’s your read on the disconnect? Are you adding into the drawdown, waiting for the long end to stabilize or staying out until the political picture clears? The best conversations on this publication happen when allocators with different time horizons and frameworks weigh in — drop your view in the comments.

Disclaimer: The content of this publication is for educational and informational purposes only and does not constitute investment advice. All investment decisions should be made in consultation with a qualified financial advisor, based on individual circumstances and risk tolerance. Valuation multiples and yield figures cited are illustrative and as-of-recent; investors should verify current data before acting. The author may hold positions in some of the securities discussed.

I’ve been trading in and out of EWZ index for a bit now. All you needed to know was that you have a big head and shoulders pattern on the chart. But the up trend is in tact.

We came back to the neck line and are up near 3% from that. Perfect retrace and that is it. Technicals told you everything you needed to know.

Great post. Only own Vale SA through the FRDM ETF. Any market cap weighted index ETF you recommend for Brail? Looks like FLBR has a low expense fee?