Deep Dive: Banco Inter ($INTR)

A Brazilian Digital Bank That Compounded From a Mortgage Shop Into a NASDAQ-Listed Super-App

The 30-Second Map

Banco Inter (NASDAQ: INTR) is the third-largest digital-native bank in Brazil by client count, 44 million users, 25.8 million of them monthly-active. It’s also one of the very few South American banks that has chosen to list its parent in the United States: the operating entity is Inter & Co, Inc., a Cayman Islands holding company that NASDAQ-listed in June 2022 and is mirrored on B3 through a 1:1 BDR (INBR32).

Today the stock trades at roughly US$6.16, a US$2.72 billion market capitalization. That puts Inter at 1.3× book value and 9.7x P/E, a multiple structure that, frankly, looks like a sleepy mid-cap incumbent rather than a digital franchise compounding net income at 35%+ YoY and approaching a 16% ROE.

This piece is a forensic fundamental walk through the company: origins, owners, governance, compensation, the five revenue engines, the full set of bank metrics, the credit book, the funding profile and the parts of the balance sheet that most retail investors skip past.

I. Origins: From Intermedium to Banco Inter (1994–2018)

The story most foreign allocators do not know is that Banco Inter is not a fintech in the Nubank sense. It is a 32-year-old bank that chose to become a fintech.

The institution was founded in 1994 in Belo Horizonte, the capital of the Brazilian state of Minas Gerais, under the name Intermedium. The founder, and still the controlling shareholder today, is Rubens Menin Teixeira de Souza. Rubens is one of the most consequential Brazilian businessmen of the last forty years and Inter is only one of his platforms. In 1979, fifteen years before founding the bank, he founded MRV Engenharia, today the largest homebuilder in Brazil by units delivered and a publicly traded company on B3 (ticker: MRVE3) where Rubens still holds 32%. He also chairs LOG Commercial Properties, CNN Brasil, the radio network Rádio Itatiaia, and the philanthropic group Movimento Bem Maior. The Menin family is also owner of the soccer club, Atlético Mineiro, a traditional club in Brazil.

For roughly its first two decades, Intermedium was a small Minas-Gerais real-estate financier with a quiet adjacent business in consumer credit. Asset base, profitability, brand, all modest. The institution operated within Brazil’s traditional banking architecture, where five incumbents (Itaú, Bradesco, Banco do Brasil, Caixa Econômica Federal, Santander Brasil) controlled roughly 85% of system assets and interchange/float economics ran in their favor.

The pivot came in 2015. Under Rubens’s son, João Vitor Menin, who had joined the bank in 2008 at age 25 and risen to CFO by 2012 and CEO by 2015, Intermedium launched what would become the first true digital-native checking account in Brazil. Zero monthly maintenance fees. Account opening fully on a smartphone, in minutes. No physical branch network. A radical model in a country where, at the time, even opening a savings account required photocopies of utility bills delivered to a branch teller.

By 2018, the digital pivot had produced enough scale and growth to take public. Banco Inter listed on B3 under the ticker BIDI11 in April of that year. Pricing day clients had grown 5×; deposits had grown 3×; and the legacy mortgage book had been recast as one product line among several. From this point onward, “Banco Inter” was no longer a regional lender. It was a national digital-banking platform with a 30-year credit-data archive that no challenger could quickly replicate.

II. The 2022 NASDAQ Migration

The next inflection point, and the one that fundamentally shapes how an outside investor underwrites Inter today, happened in June 2022.

In a structurally important corporate restructuring, Banco Inter migrated its parent into a Cayman Islands holding company called Inter & Co, Inc. The Brazilian operating bank,. Banco Inter S.A., became a subsidiary. The Cayman parent dual-listed: an ordinary listing on NASDAQ under the ticker INTR, and a 1:1 mirror BDR on B3 under INBR32.

The share-class structure is what every minority shareholder should understand:

Class A common shares: one vote per share. These are the publicly traded shares, on NASDAQ and via B3 BDRs. Approximately 50% of economic equity sits in Class A free float.

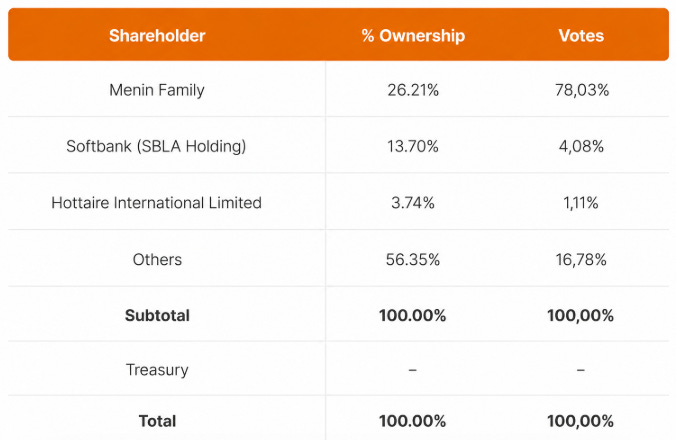

Class B common shares: ten votes per share. These are held by the founding Menin family and a small group of related parties. They are not publicly tradable.

The Menin family’s beneficial ownership is approximately 27% of economic equity but, because of the 10:1 voting ratio on Class B, they retain decisive voting control. The remaining major shareholder is SoftBank Group, which holds approximately 15% of economic equity through Class A shares, a position dating back to a pre-IPO private placement.

A protective covenant in the structure: if Class B shares fall below 10% of total shares outstanding, they convert 1:1 into Class A. In other words, family control is contractually durable through any realistic dilution scenario.

This is the single most important governance fact in the file. Class A holders cannot replace the board. They cannot mount an activist campaign. They cannot force a sale. The Menin family controls Inter; Class A holders ride.

Whether that’s a feature or a bug depends entirely on the alignment math, which we will get to in the compensation section.

III. Ownership Map at a Glance

Free float concentration is therefore meaningful, daily trading volume on INTR runs in the US$15–30M range and the practical free float available to institutional allocators is below the headline 50% figure once strategic holders and lock-ups are accounted for.

IV. The Board and Senior Management

Inter & Co’s board has nine members. The structure is meaningfully more “founder-controlled” than the average S2-tier Brazilian bank board, but the seat composition includes credible institutional voices and at least one industry heavyweight.

Rubens Menin — Chairman. The cultural anchor and the controlling voice.

João Vitor Menin — Global CEO of Inter & Co since July 2024 and board member. Rubens’s son. Joined the bank in 2008 at 25, made CFO at 29, CEO at 32, NASDAQ-migration architect at 38, Global CEO at 41. He has been the operational force behind every consequential strategic decision over the last decade: the 2015 digital pivot, the 2018 IPO, the 2022 Cayman migration, the 60-30-30 Plan (will explain later) unveiled in January 2023, and the Rule of 50 (will explain later) strategy update articulated at Owners’ Day on May 11, 2026.

Alexandre Riccio — CEO Banco Inter Brasil (the Brazilian operating bank) since July 2024. Career banker. Previously CFO of Banco Original (JBS owned); before that, Head of Corporate Banking at Bradesco. The Riccio appointment is one of the most informative signals about how the Menin family thinks about its own succession: João Vitor moved up to Global CEO, but the Brazilian operating bank was handed to a non-family, non-founder professional banker. Operational discipline, not founder romance.

Santiago Stel — Senior Vice President and CFO. Argentine-Brazilian. Joined in 2023 from BTG Pactual, where he was Head of Investor Relations. Stel has been a critical hire: he has methodically upgraded Inter’s disclosure quality, KPI consistency, and quarterly cadence to the standard that U.S. institutional investors expect. Anyone who has read Inter’s quarterly releases pre-2023 and post-2023 will see the difference immediately.

Independent directors include Cristiano Maron, a former Itaú executive who brings traditional-banking depth, and André Esteves, the founder of BTG Pactual, in an observer/strategic-advisor role.

A cultural detail that matters for retention and operational continuity: Inter’s senior leadership is concentrated in Belo Horizonte, not São Paulo. The cost of living is lower, the talent market is less mercenary, and tenure tends to be longer. For a Brazilian financial company this is a real asset; the average São Paulo banker rotates between Itaú, BTG, and a buy-side seat every 30 months.

V. Executive Compensation and Alignment

Inter operates a Long-Term Incentive Plan (ILP) that is heavily weighted toward equity, stock options and restricted shares, rather than cash bonuses.

The 2026 Annual General Meeting approved a total compensation budget of US$29.9 million for all directors and officers, versus US$20.6 million in 2025. The step-up reflects team expansion (the U.S. branch infrastructure post the January 2026 Federal Reserve licensing) and equity-grant pricing.

The critical alignment feature: vesting on the ILP is explicitly tied to the 60-30-30 Plan KPIs — 60 million clients, 30% ROE, and 30% efficiency ratio by 2027. Senior executives only collect equity grants if these targets are hit. This is not unusual in U.S. tech, but is rare in Brazilian banking, where compensation has historically been a function of seniority and tenure rather than enterprise outcomes.

The disclosure that Inter’s IR team is most proud of: senior executives collectively hold more INTR shares than they have received in cash compensation over their full tenures. Insider ownership at Inter is materially above the level at any major Brazilian incumbent, where insider equity ownership is typically single-digit percentage and the C-suite is salary-driven.

Three concerns worth flagging on governance, in the interest of intellectual honesty:

Family control via Class B super-vote. Working well so far. Limits strategic optionality (no hostile takeover, no activism). A bull would call this stability; a bear would call this trapped capital.

Related-party transactions. The Menin family controls MRV, LOG, CNN Brasil, and other entities. Inter discloses business relationships with several. Disclosure quality has improved but ongoing monitoring is warranted.

Acquisitive history. Inter has acquired several smaller assets — USEND (cross-border payments), Pronto! (digital lending), IDTech (identity), among others. Goodwill on the balance sheet is R$2.1 billion, roughly 20% of equity. Not extreme, but a number to track for impairment.

VI. The Five Revenue Engines

The single best frame for understanding the modern Banco Inter is that it is a vertically integrated super-app, with five complementary income engines living inside one mobile experience. Management describes this as “Inter by Design.” From an outside-in view:

Engine 1 — Banking & Credit (65% of revenue)

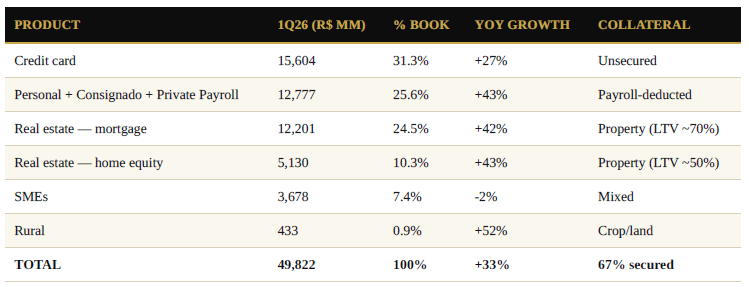

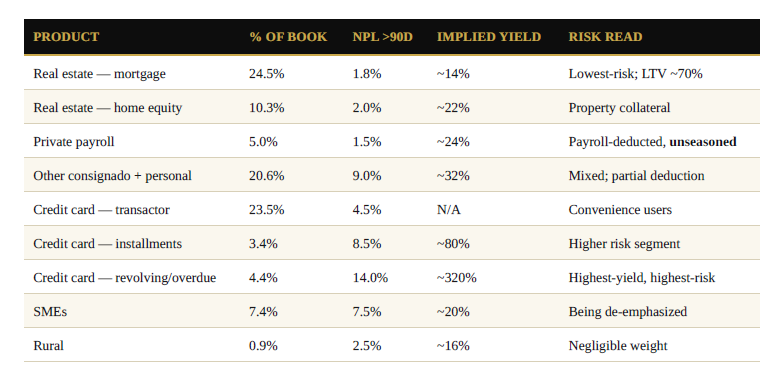

The loan portfolio at the end of 1Q26 was R$49.8 billion, growing 33% year-on-year, roughly 3× the pace of the Brazilian banking system. Six product lines, in descending order of book:

The mix story matters more than the headline growth. A year ago, secured assets (mortgage + home equity + payroll-deducted personal) were roughly 60% of the book. Today they are 67%. Private payroll, collateralized through automatic deduction from employee paychecks under cooperation agreements with employers, has grown from R$0.2 billion to R$2.5 billion in 12 months. That is a 12-fold expansion of a new product line, and as we will discuss in the credit section, it is one of the largest underwriting unknowns in the file.

Engine 2 — Inter Invest (15% of fee income)

R$184 billion in Assets under Custody at 1Q26, growing 26% YoY. Inter Invest is a self-directed retail brokerage embedded in the same super-app: equities, fixed income, ETFs, BDRs, multimarket funds, plus Inter Asset Management’s proprietary product set. The platform earns management fees on AuC and brokerage on trading, and, importantly, it consumes almost no balance sheet. Fee income flows directly to ROE.

Operationally, Inter Invest is the closest competitor to XP and to BTG’s retail platform, but distributed through the banking app of a 44-million-client universe.

Engine 3 — Inter Seguros (Insurance Brokerage)

1.5 million+ active insurance policies in force. Inter Seguros distributes third-party products: life, residential, auto, travel, dental, pet. They earn brokerage commission plus a layer of digital servicing revenue. At the unit-economic level, this is the highest-margin business line at Inter; insurance brokerage is a 30–40% net margin business globally, and Inter’s distribution-cost advantage (already-acquired bank customers) pushes the unit margin even higher.

Engine 4 — Inter Shop & Commerce Plus (Marketplace)

This is the engine that has no parallel at any other Brazilian bank. Inter Shop is a marketplace embedded inside the bank app, where 5,000+ retail partners pay Inter a take rate to access its 26 million monthly-active customers. Quarterly GMV of R$1.2 billion in 1Q26 (down from R$1.5 billion in 4Q25 on a soft seasonal comp). Customers earn cashback through Inter Loop, the loyalty program, R$53 million in cashback paid in 1Q26, a deliberate marketing spend that anchors transactional behavior on the Inter card.

Inter Shop is also, indirectly, a payment-instrument acquisition machine. Customers shop, spend on Inter cards, generate interchange.

Engine 5 — Global Services (Inter Global Account)

A USD-denominated account product for Brazilian clients (and now, post the January 2026 Federal Reserve and Florida OFR branch approval, also for U.S. clients). Approximately 5 million Global Account customers. Revenue drivers: FX spread on conversions, international interchange on USD card spend, remittance fees, and, over time ,a meaningful float opportunity as the average USD balance per account grows.

The Miami branch is the most interesting strategic optionality in the entire Inter equity story. A regulated U.S. banking branch is an asset that takes Brazilian challengers years to replicate; it gives Inter cross-border banking capability that, properly executed, could push the Global business from a fee-light add-on to a meaningful P&L line by 2028–29.

VII. Unit Economics — The Cleanest Lens

The most disciplined way to understand a digital bank is per-customer unit economics, and Inter discloses them quarterly with unusual granularity.

ARPAC = Average Revenue Per Active Customer. The mature-cohort (1Q21 vintage) ARPAC is R$133 / month, 133% above the blended figure. As cohorts age and Inter cross-sells through the “Account → Spend → Invest → Borrow” funnel, ARPAC roughly 2.3× by year-five of a customer’s tenure, while Cost-to-Serve stays approximately flat. This is the textbook digital-bank operating leverage curve.

A second engagement metric that anchors the moat conversation: 69% of Inter’s active clients use Inter as their primary banking relationship, meaning at least 50% of post-tax income flows through the Inter account during the month. NPS of 85 is in the “Excellence Zone” and ahead of every Brazilian incumbent (Itaú, Bradesco, and Santander typically print NPS in the 30–50 range).

Transaction volume context: R$427 billion in TPV (Pix + cards) in 1Q26, 20.8 million daily logins, 30 million financial transactions per day. Pix market share approximately 9% of brazilian total market.

Pix is an instant electronic payment method created by the Central Bank of Brazil, which allows money transfers in a few seconds, at any time of the day, in a practical and secure way. The concept can be explained as an ‘instant payment’.

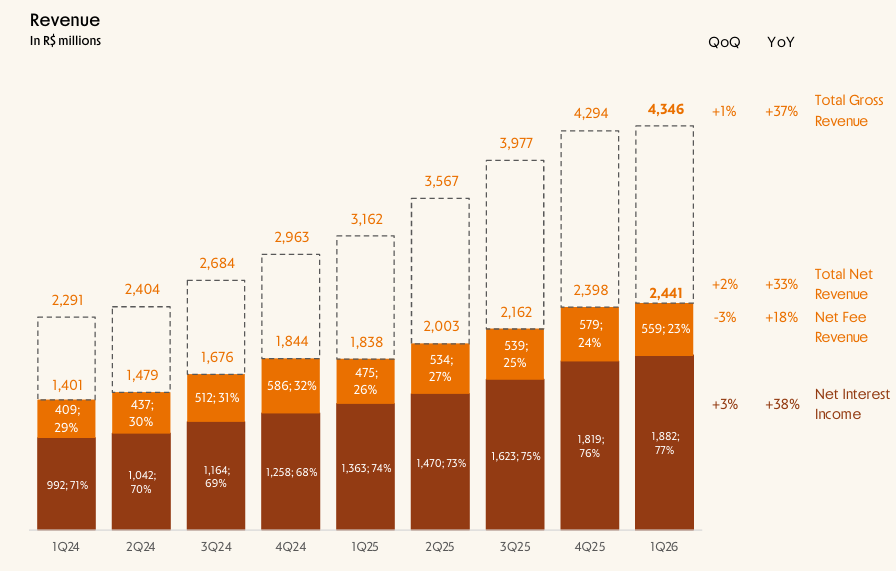

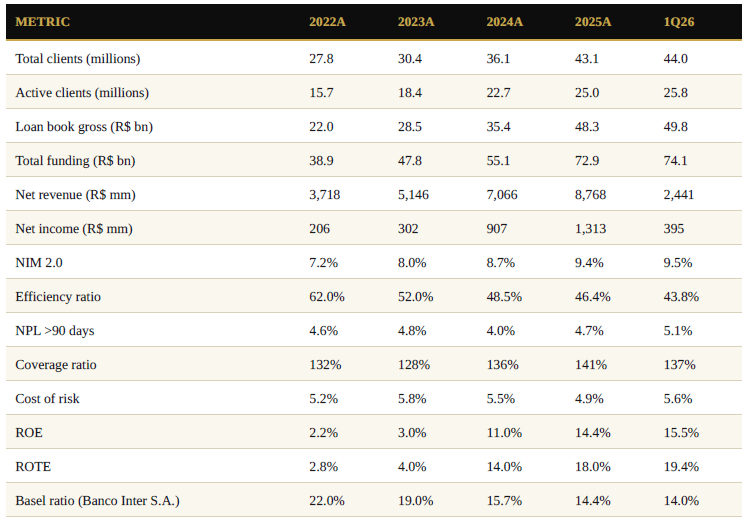

VIII. The Full Financial Trajectory (2022–1Q26)

This is the data table everyone should print and put next to the screen.

Three observations on this table.

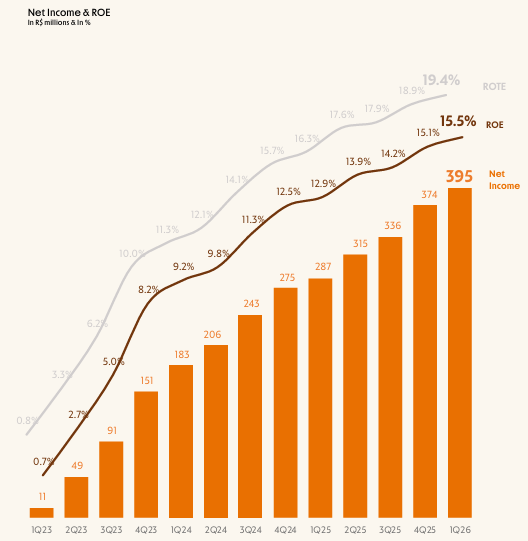

1)ROE trajectory. Inter posted a 2.2% ROE in 2022 and a 15.5% ROE in 1Q26. A 13-percentage-point improvement in 4 years is not normal for a bank. The drivers are (a) the funding-cost edge widening as the deposit base grew; (b) operating leverage as the cost base barely moved while revenue compounded; and (c) the loan-book mix shifting toward higher-yielding products (private payroll, credit card revolving) and away from low-margin SME and lower-yielding mortgage exposure.

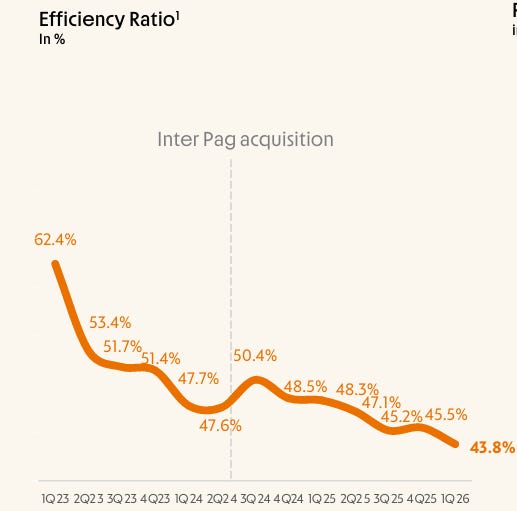

2)Efficiency ratio. From 62% in 2022 to 43.8% in 1Q26. This is the single most important operational signal in the file. Management has guided to a 30% efficiency ratio by 2027, implausibly aggressive in absolute terms (Itaú is at 39.5%; even BTG Pactual sits at 35%), but the directional improvement is real and visible. Revenue grew 33% YoY in 1Q26 against operating expense growth of 20%. That 13-percentage-point operating-leverage gap is what is driving the efficiency-ratio compression and is, in my view, the most defensible bullish driver in the entire equity story, because it requires no macro tailwind to continue.

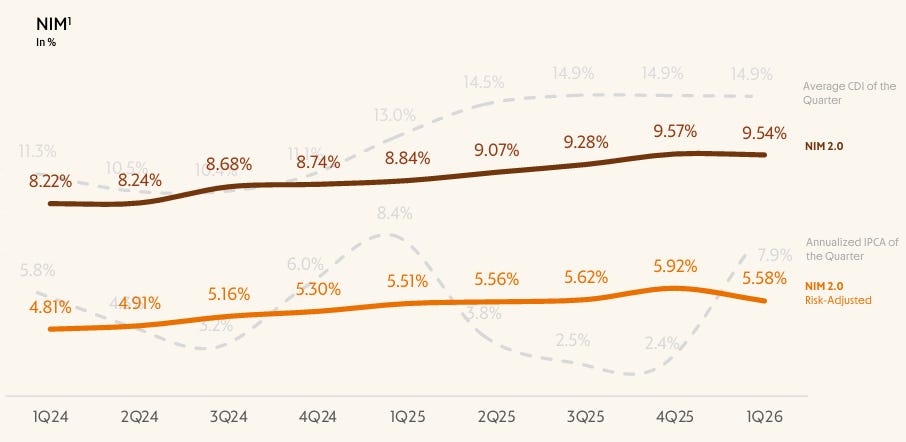

3)NIM expansion. NIM 2.0 (Inter’s preferred measure: interest income over average remunerated portfolio) reached 9.54% in 1Q26, within 3 basis points of the all-time high. Two structural drivers: high Brazilian benchmark rate (interest rate at 14.50%) lifting the asset yield on the R$50bn loan book, and a sub-system funding cost of 64.1% of the interest rate (more on this below).

IX. The Funding-Cost Edge

This is the most underappreciated structural advantage in the Inter story, and a feature that, in my view, deserves more attention than it gets from sell-side coverage.

Brazilian benchmark interest rate (Selic) averaged ~14% in 1Q26. A standard incumbent retail bank pays its depositors approximately 85% of CDI (the interbank rate, which moves with Selic). That is the system average. Inter paid 64.1% of CDI in 1Q26.

The 21-percentage-point gap on the cost of funding compounds across the deposit base. With R$74.1 billion in total funding, every 100 bps of funding-cost edge is worth roughly R$740 million annually in NII versus a peer paying system-average rates. The actual edge is approximately 200 bps, so we are talking about a structural NIM advantage worth in the order of R$1.5 billion annually, call it 40% of Inter’s full-year 2025 net income.

Why is Inter paying so much less? Two structural reasons:

R$19 billion (26%) of the funding base is in non-interest-bearing transactional deposits. Checking-account balances earning zero. Customers leave money in these accounts because the super-app is convenient for bills, transfers, Pix, cards. The functional value of the account replaces the interest the customer would otherwise demand.

R$9.4 billion in “Meu Porquinho”, the digital piggy bank where customers park savings. Earns below-CDI rates. 5+ million customers participate.

Both of these features compound with client growth at zero marginal cost. As Inter adds clients, the funding base grows automatically and at a blended cost meaningfully below what any new digital challenger could match without building the same multi-year primary-banking relationship.

This is not a moat in the Buffett “wide and unassailable” sense. Other banks have low-cost transactional deposits too. But Inter’s combination of cost-of-funding edge plus primary-banking-relationship penetration (69%) plus a 30-year credit-data archive plus the super-app cross-sell engine is the kind of layered advantage that takes a competitor a decade and several billion in spend to replicate.

X. The Loan Book Up Close

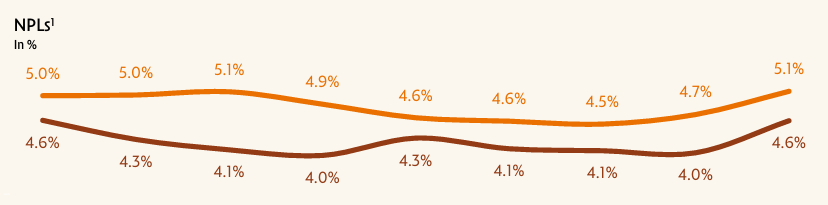

Inter discloses NPL by product line, and the resulting picture is more nuanced than the headline 5.1% NPL >90d number suggests.

Two things stand out.

The revolving credit-card line is paying ~320% annualized yields with 14% NPL >90d. This is not a typo. Brazilian credit-card revolving is the most punitively priced lending product in the world, structurally a function of BCB-mandated mandatory revolving access plus high system delinquency. It generates extraordinary risk-adjusted yields when properly underwritten, and is one of the reasons Inter’s risk-adjusted NIM stays attractive even at 5.6% cost of risk.

Private payroll is the single largest underwriting unknown in the file. The book has grown from R$0.2 billion to R$2.5 billion in twelve months, a 12× expansion. The collateral structure (automatic deduction from paychecks at the employer level) materially limits loss-given-default. But no Brazilian bank in modern history has grown a new product line at this pace without an eventual credit-quality surprise. The vintage is unseasoned. The NPL print on this book is currently 1.5%, but that is exactly what you would expect from a portfolio dominated by 6-month-old originations. The next 12–18 months are when this number tells you something.

Management raised cost-of-risk guidance from 5.0–5.5% to ~6.0% for the remainder of 2026 at the 1Q26 results release. NPL >90d ticked up 50 bps QoQ to 5.1%. The early-warning indicator, NPL 15-90 days, moved up 60 bps QoQ to 4.6%. Coverage ratio fell to 137% from 141%. All three of those numbers are moving in the wrong direction simultaneously.

The bull rebuttal, and I am presenting both sides honestly, is that (a) the cost-of-risk increase reflects deliberate portfolio mix shift toward higher-yielding products where risk-adjusted economics are still attractive; (b) the Brazilian credit cycle typically inflects 6–12 months ahead of system NPL, meaning the worst could be priced in by 2027; (c) the coverage ratio at 137% is still meaningfully above the Brazilian banking system average of 110%.

The stress-test in the model: if NPL >90d rises to 9% and loss-given-default reaches 60%, expected losses would consume the current allowance with a roughly R$400 million gap to equity, a 4% hit to book value. Only at NPL >12% (a Global-Financial-Crisis-like scenario) does equity face material impairment of approximately 10% of book. Given the secured-asset mix at 67%, that tail scenario is low-probability.

XI. Capital, Funding, and the R$2.1 Billion Hiding at Cayman

Two capital figures matter, and they are not the same number.

Banco Inter S.A. Basel ratio (the operating bank): 14.0% at 1Q26, with Tier 1 CET1 at 12.1%. Well above the 9.5% regulatory minimum for an S2-classified institution. Inter has been proactively topping up Tier 1: R$500 million perpetual subordinated bonds in April 2025 and a further R$300 million perpetual Tier 1 notes in April 2026 (expected impact roughly +70 bps Basel).

Inter & Co holding (Cayman) excess capital: approximately R$2.1 billion sitting at the parent, outside the Banco Inter S.A. Basel calculation. This is real, deployable capital. Optionality includes (a) buybacks of INTR, (b) M&A in fintech or adjacent verticals, (c) further capitalization of Banco Inter S.A. as the loan book scales, or (d) capitalization of the U.S. branch as that ramps.

That R$2.1 billion is approximately 21% of consolidated equity. It’s not reflected anywhere in the Basel ratio at the operating-bank level, and it’s structurally available to the company. For an outside-in analyst, this is the kind of detail that does not show up in screeners but matters for the intrinsic valuation.

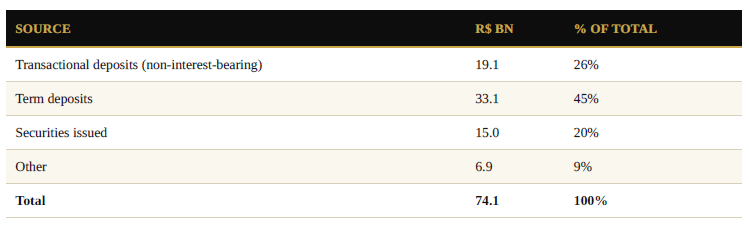

Funding mix at 1Q26:

The loan-to-deposit ratio reached 92% in 1Q26, meaningfully higher than the 70% level Inter was running in 2022. Translation: Inter is now operating much closer to a "real bank" stance (deploying deposits into loans, accepting maturity transformation risk) and less like the deposit-rich, asset-light marketplace it was three years ago. This is one of the most important structural facts about today's Inter that the equity narrative often understates.

XII. What Retail Investors Don’t Look At

Five balance-sheet items that materially change the underwriting and rarely make it into the investor decks.

1. Deferred Tax Assets — R$1.9 billion. Recognizable only against future taxable profit. At a 25% effective tax rate, monetizing the full DTA requires approximately R$7.7 billion of cumulative pre-tax income. achievable over 4–5 years at current trajectory, but not guaranteed. A conservative valuation should haircut 30–50%.

2. Off-balance-sheet receivables anticipation — approximately R$5 billion. Inter funds credit-card receivables partly through anticipation programs (disclosed in Note 9.a). This is securitization-style funding; efficient but adds a layer of leverage that is not reflected in the headline metrics. True leverage on a look-through basis is roughly 0.5× higher than the on-balance number suggests.

3. Coverage ratio erosion — 143% → 137% over four quarters. This is either evidence of more efficient provisioning OR evidence of quiet under-provisioning of the private-payroll vintage. The next two quarters of coverage data will tell you which story is right.

4. Private payroll — R$0.2bn → R$2.5bn in twelve months. The 12× growth is unprecedented at this scale in modern Brazilian banking. Payroll-deduction collateral materially limits LGD, but the unseasoned vintage means the reported NPL on this book is not yet informative.

5. Holding excess capital — R$2.1 billion. Discussed above. The single largest piece of valuation optionality in the file.

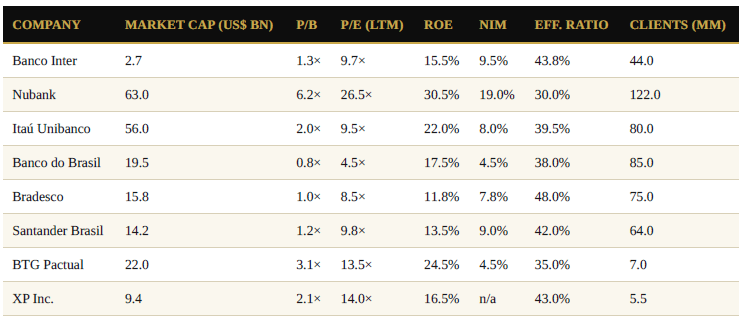

XIII. Peer Positioning

Inter does not have a perfect comparable. Nubank is far larger (122 million clients, US$63 billion market cap, 30% ROE). The Brazilian incumbents are slower-growing and trade at incumbent multiples. BTG Pactual is closest operationally (24.5% ROE, 35% efficiency ratio) but is a different mix of businesses.

Read this table the way the market reads it. Inter’s multiples (1.3× P/B, 9.7× P/E) cluster with Bradesco and Santander Brasil, both legacy incumbents with low-teens ROE, single-digit growth, and minimal optionality. They do not cluster with BTG, XP, or Nubank, the three names that operationally most resemble Inter’s mix and growth.

Whether that is mispricing (the bull case) or an accurate read of execution risk and governance (the bear case) is the central question of any Inter thesis.

XIV. The 60-30-30 Plan and the Rule of 50

Management’s two strategic frameworks deserve to be in any deep dive.

60-30-30 Plan, articulated at Owners’ Day in January 2023 and reaffirmed every Owners’ Day since: 60 million clients, 30% ROE, 30% efficiency ratio by 2027.

Clients: 44M at 1Q26 → needs ~16M net adds in 21 months. On current ~7M/year run-rate, achievable.

ROE: 15.5% at 1Q26 → needs +1,450 bps in 21 months. The most ambitious leg of the plan; current trajectory suggests this slips to 2028 or 2029.

Efficiency ratio: 43.8% at 1Q26 → needs -1,380 bps. On current trajectory of ~400 bps/year improvement, on schedule.

Rule of 50, articulated at Owners’ Day on May 11, 2026: revenue growth + ROE ≥ 50% as the steady-state north star. At 1Q26 this metric is roughly 33% + 15.5% = 48.5%. Within one percentage point of the target.

The Rule of 50 is, in my reading, a softer reframing of 60-30-30, recognition that the original ROE target (30%) may not be hit in 2027 but that the bank should still compound through a combination of growth and profitability that puts the equity story in the same neighborhood. It’s also more honest about the tradeoffs: if Inter wanted to accelerate ROE today, it could pull back loan growth and lever up the existing book; instead management is choosing to keep growing the franchise and accept a longer ROE ramp.

Medium-term ROE guidance disclosed at Owners’ Day 2026: 26–30% by 2029.

XV. The Bear Case

In the interest of intellectual honesty and because finance Substack readers (correctly) distrust pieces that only present the bull side, here is the bear case:

Cost of risk is inflecting. NPL 90d, NPL 15-90d, and coverage are all moving against the bank simultaneously for the first time in three years.

Private payroll is an unseasoned, fast-growing book. The next 12–18 months will tell whether the underwriting quality is real.

Class B family control limits minority remedies. No activism, no hostile takeover, no shareholder forcing function.

Multiple expansion requires sustained ROE improvement. If ROE stalls at 16–18%, the equity story compresses to incumbent multiples and the re-rating thesis does not work.

Concentration risk. Roughly 31% of the loan book is unsecured credit-card receivables, where cost of risk is highly sensitive to the Brazilian consumer cycle.

U.S. branch execution is unproven. The Miami license is real; the revenue from the U.S. business is not yet meaningful.

XVI. The Strategic Optionality

And to complete the picture, the upside-only catalysts that an Inter shareholder is paying for at 1.3× book:

Operating leverage continues — efficiency ratio compounds toward 35% by 2028 even without macro tailwind.

U.S. branch becomes a real P&L line by 2027–28. Cross-border banking is a moat that does not exist at any Brazilian challenger.

Seven AI scales. The multi-agent AI launched in 1Q26 industrialized customer interactions; if it delivers the cost-to-serve compression management has discussed (R$13 → R$10 per active customer/month), efficiency improves by another ~300 bps without revenue effort.

Funding-cost edge widens further as transactional deposit base grows with client count.

R$2.1 billion holding capital is deployed — buybacks at 1.3× book are immediately accretive; M&A in adjacent verticals adds optionality.

XVII. What I Personally Watch Each Quarter

For anyone tracking this name actively, these are the eight numbers I check first in each release:

NPL 15-90 days — the leading indicator. If it accelerates past 5.0%, the bear case strengthens materially.

Cost of risk realized vs. 6% guidance. Credibility test for management.

Coverage ratio. A floor at 135% is acceptable; below that is concerning.

Efficiency ratio. Must keep moving toward 40% by end-2026 to be on the 60-30-30 path.

Private payroll book growth and NPL. If the NPL on this line stays below 2% through 2026, the bull case on this product is validated.

Active rate. Currently 58.6%; trending should be toward 62–65% as cohorts mature.

Loop cashback as % of revenue. Marketing spend efficiency. Currently 6% of fee income; rising would signal customer-acquisition pressure.

U.S. branch contribution to revenue. Material number expected by 2H26.

Closing

Inter is, in my reading, a quality digital-banking franchise priced like a sleepy Brazilian incumbent. The numbers themselves are not in dispute, 44 million clients, R$50 billion loan book, 67% secured, 64% of CDI funding cost, 15.5% ROE, 43.8% efficiency ratio. Those are facts.

What is in dispute is whether the next leg of the compounding, the path from 15.5% ROE to the 26–30% ROE that management has guided to by 2029, is delivered, delayed, or never reached.

If you believe management’s plan and the operating-leverage engine continues to grind, the current multiple is incongruent with the trajectory. If you believe cost of risk is signaling something darker, the current multiple is fair and the next 12 months may not be pleasant.

I don’t have a buy or sell call for this piece, that is not what a fundamental anatomy is for. What I do have is the data, the structure, the governance map, and the questions worth asking before you take a position one way or the other.

If this was useful, share it with one allocator who does not yet have Brazilian digital banks on their radar. The setup is getting interesting.

Disclaimer: The content of this publication is for educational and informational purposes only and does not constitute investment advice. All investment decisions should be made in consultation with a qualified financial advisor, based on individual circumstances and risk tolerance. Valuation multiples and yield figures cited are illustrative and as-of-recent; investors should verify current data before acting. The author may hold positions in some of the securities discussed

Sources: Inter & Co quarterly results releases (1Q22–1Q26), SEC 20-F filings, Inter & Co investor presentations including Owners’ Day 2026 (May 11, 2026), Bacen disclosures, peer comparables compiled from public filings.